The number of operators investing in standalone 5G networks globally is growing at a snail’s pace, newly published market statistics show.

This is perhaps something of a concern for an industry searching for the right formula for the monetisation of hefty 5G investments; without 5G SA, operators’ opportunities are limited to faster mobile data speeds.

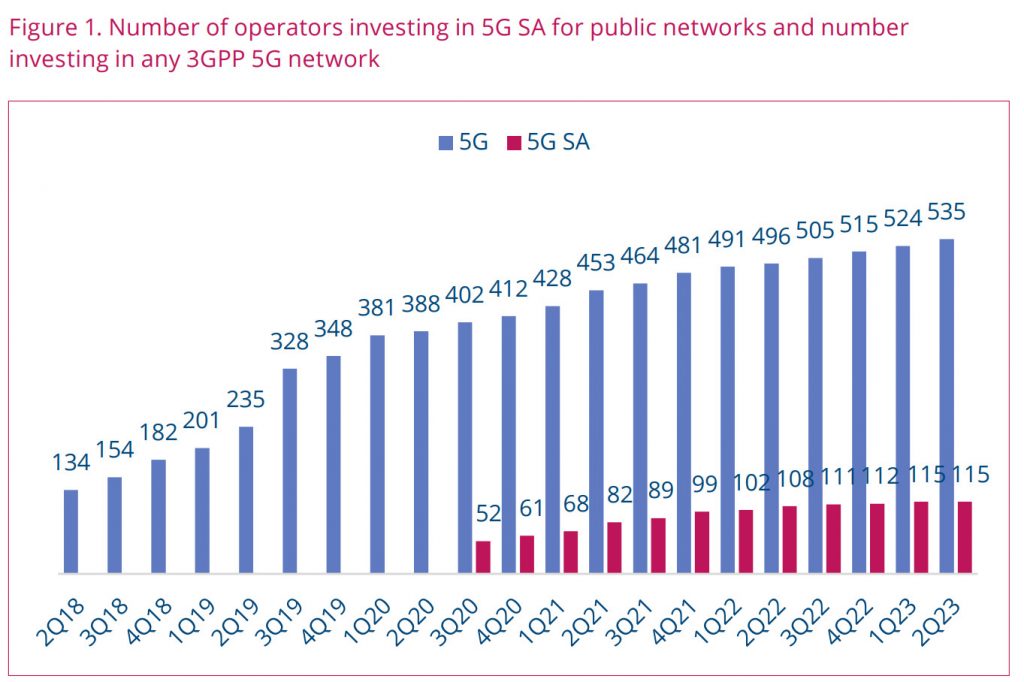

That’s not to say there is no 5G SA out there, of course. The latest numbers from the Global mobile Suppliers Association (GSA) covering the second quarter of this year show that 115 operators in 52 countries have been investing in public 5G SA. The trouble is, that’s exactly the same figure the industry body came up with in Q1, and an increase of just three on end-2022 (see chart).

Furthermore, the figures refer not only to real-world deployments, but also planned rollouts and 5G SA trials.

36 operators have launched or deployed public 5G SA networks, including two soft launches, the GSA added. That’s one more than the firm catalogued in its previous quarterly update, although it has amended a couple of figures since then, so it’s difficult to gauge any progress there.

However, announcements from the industry paint a slightly different picture.

New Zealand’s Spark last month announced that it will spend up to NZ$60 million ($37.5 million) over the next three years upgrading its 5G network to SA, naming Ericsson and Red Hat as its vendors of choice. And a month earlier Vodafone flipped the switch on 5G Ultra in the UK, its standalone offering re-badged to appeal to the masses.

So it could be that an uptick in 5G SA – particularly from operators moving from trials to launch – is on the way. Indeed, while the GSA does not make any hard predictions on that front, it is upbeat about the future.

Based on the number of operators testing or piloting the technology, it believes that “launches of 5G SA look set to continue apace,” which would be good news from the monetisation angle.

However, the GSA has identified a fair number of organisations using 5G SA for private networks, which potentially – depending on the deployment model – takes business away from the telcos. As of May there were well over 1,000 organisations known to be deploying LTE or 5G private mobile networks, or known to have been granted licences to do so. Of them, 505 were using 5G – not including so-called 5G-ready networks – and 66 of those were already working with 5G SA.

They include manufacturers, academic organisations, commercial research institutes, construction, communications and IT services, rail and aviation organisations, the GSA said.

The mobile operators will do their best to ensure they are not left out in the cold though. This week, for example, the UK’s Virgin Media O2 launched what it claims is the first portable commercial 5G SA private network, the idea being to simplify the whole thing for enterprise customers.

So, while the reality of 5G SA might be yet to match the hype, the headline figures perhaps do not tell the full story either.

The GSA sums up its latest findings thusly:

“The market is seeing the emergence of a strong 5G SA ecosystem with chipsets, devices of many types and users of public as well as private networks. We can expect to see the market go from strength to strength.”

Original article can be seen at: