Public cloud providers offer telecom operators a radical business transformation opportunity but many remain wary of relinquishing their assets and forsaking control.

Today, public cloud providers have accelerated time-to-market for many enterprises. With 5G core networks considered inherently cloud-native, many 5G standalone networks are being deployed with a cloud-based architecture. Meanwhile, concerns remain over the suitability of public cloud for operator network infrastructure and workloads.

This article sets out to explore what communication service providers (CSPs) and other industry experts consider some of the biggest challenges and drivers for the adoption of public cloud.

CSP Drivers

With telcos’ growing need to expand revenues beyond connectivity, research from analyst firm STL Partners suggests there is an opportunity for operators to capitalise on the cloud and to partner with public cloud providers. As such, the analysts suggest the migration of IT environments and telco workloads to the public cloud are inevitable for operators.

Further, a recent study by Capgemini, an IT services and consulting firm, shows that on average CSPs are expected to invest around one billion US dollars into their network cloud transformation over the next 3-5 years. Per operator, this sum reportedly equals to 38-44% of their total network transformation budgets.

With such level of investment needed to develop a cloud platform, applications, and services, combined with the opportunity to capitalise from public cloud, some in the industry see hyperscalers and other large public cloud vendors as ideal partners for CSPs. The existing investments into building and operating large cloud infrastructures and offerings can significantly reduce their total cost of ownership (TCO) for CSPs, making TCO the primary driver for telcos to embrace public cloud.

Operational efficiencies gained from running IT systems on the public cloud are another area often discussed in relation with drivers for moving workloads. In terms of scale, public cloud is believed to enable CSPs to expand their addressable market, improve their B2B offerings, and support B2B2x solutions.

Public cloud also promises to offer a pay-as-you-go model based on microservices and Kubernetes (also known as k8s) applications. Such microservices enable telcos with rapid deployment of their go-to-market strategies and facilitate real-time data streaming. Though it is worth noting here that k8s can also be deployed in an on-premise environment and as such are not unique to public cloud.

Public cloud also offers deployment benefits such as flexible and agile customer and revenue management and scalable offerings to increase monetisation of services. Therefore, hosting business support systems (BSS) and the operating support systems (OSS) in the public cloud are seen as particularly valuable use cases. However, there are also security considerations when hosting transactional data and systems (i.e. BSS workloads) on the public cloud. This is due to its multitenancy nature (more to this further below).

In terms of leveraging additional public cloud capabilities, research from Omdia suggests that there are additional advantages for CSPs. These include capabilities offered by AI and ML to help automate processes and monetise insights gained through data. Here Google’s Cloud Platform is cited as the frontrunner. Automation is valuable to CSP tasks such as testing and repetitive tasks, though the research is also quick to flag that maintaining control is equally important for operators.

Some may argue public cloud is an attractive proposition especially for new market entrants. In the US, greenfield operator Dish presents such an example. In early 2021 it announced a collaboration with Amazon Web Services (AWS) for constructing its full 5G network. The operator connected all its 5G hardware and network management systems through the cloud provider.

There are also public cloud partnership examples between hyperscalers and brownfield operators. These include AT&T and Microsoft Azure in the US, Bell Canada and Google, and more recently Tele2 and AWS in Norway. But despite some uptake in such partnerships, many operators remain somewhat sceptical and unclear about the best approaches towards public cloud. Here are some of the key concerns we have gathered.

CSP concerns over public cloud

The telecom industry is highly regulated and often considered as part of critical infrastructure. As such, it is vital that CSPs maintain control, know where their networks and customer data reside, and can ensure those locations are safe.

In a recent survey by Telecoms.com more than four in five industry respondents feared security concerns over running telco applications in the public cloud, including 37% who find it hard to make the business case for public cloud as private cloud remains vital in addressing security issues. This also means that any efficiency gains are offset by the IT environment and the network running over two cloud types.

Meanwhile, many in the industry also fear vendor lock-in and lack of orchestration from public cloud providers. Around a third of industry experts from the same survey find it a compelling reason not to embrace and move workloads to the public cloud unless applications can run on all versions of public cloud and are portable among cloud vendors.

This brings us to the issue of interoperability and interconnectedness. Proponents of public cloud may argue that through a multi-cloud approach operators can use offerings from various vendors and thus introduce a diverse set of public cloud providers in their networks. However, as it stands, the services of different public cloud vendors are indeed not interconnected nor interoperable for the same types of workloads. This concern is one of the drivers to avoid public cloud, according to some operators.

Alongside vendor lock-in and interoperability are also considerations over TCO savings versus long-term costs. In that, CSPs are unclear over the long-term financial benefits and worry over potential risks of increased costs once their network is locked-in with a public cloud provider.

When it comes to network or service availability, there is still a lack of reliability on hyperscalers for five nines (a telecom network uptime goal of 99.999% of the time), according to some voices in the industry. As critical infrastructure, service availability (which contractually is typically defined under a service level agreement) is a hugely significant characteristic for network operators. Network availability can also have a significant impact on operators both commercially as well as from a customer experience perspective.

As an increasing number of mission critical application and services are added on telecom networks, the ability to support five nine KPIs and delivering on service level agreements becomes even more critical. Collaborations among vendors and public cloud providers can help optimise platforms and support network availability.

These concerns are also evident by the recent operator-driven initiative Sylva. It’s been argued that the project highlights the operator community’s keenness on taking telco cloud into own hands. The initiative also highlights, alongside security, data sovereignty as another key area of concern for CSPs. This further emphasizes the need for alternative solutions to public cloud that are built with open, interoperable, and interconnected solutions in mind has moved up CSPs’ priority list.

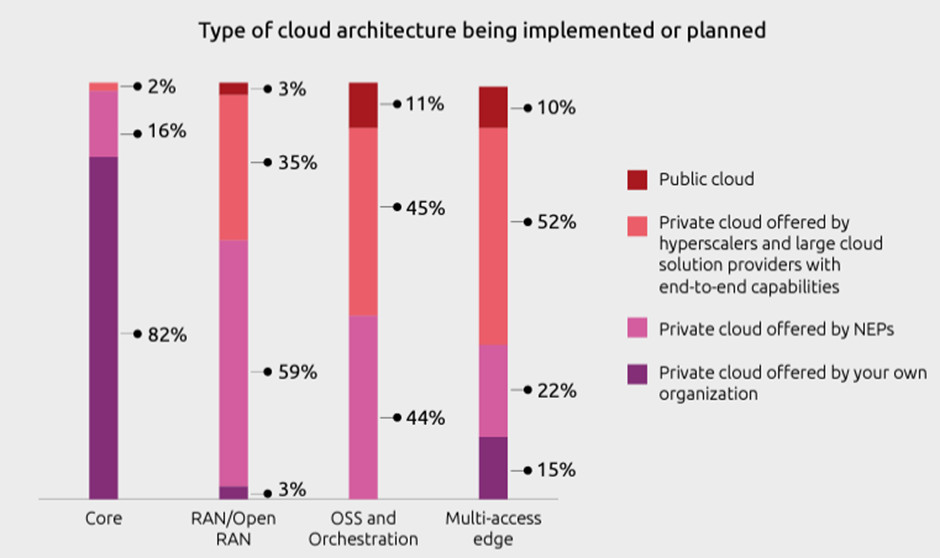

Considering these challenges, it is not surprising to see that public cloud still makes up a small portion of total telecoms networks and workloads. The below graph from a research paper by Capgemini illustrates which type of cloud architecture is currently being used or is planned in the telecoms core network, the Radio Access Network (RAN), OSS and orchestration, and for the use of multi-access edge computing.

Source: Capgemini

Hybrid cloud could ease the transition

With 5G core leading the migration of network workloads to the cloud, it is more important than ever to find the optimum road to cloud adoption. Many in the industry are considering a balanced approach in their journey towards becoming cloud-native. In that, hybrid cloud enables CSPs to identify the best use cases for each cloud strategy and thus to transition telco applications and workloads more gradually and systematically. It also allows CSPs to consume public cloud applications and benefits in a private manner.

For instance, in a bid to modernise its BSS to match the capabilities of its e-commerce and application offerings, European CSP Vodafone entered into a partnership deal with cloud solutions provider Oracle last year. Here, due to the risks associated with transactional data hosted on the public cloud, the operator opted for a hybrid model. As such, Oracle has built the operator a complete set of public cloud offering on the CSP’s own data centres, i.e. keeping the workloads on-premise.

The operator also has several hybrid cloud partnership agreements with the other US-based hyperscalers for its operating support systems, data processing and analytics, and edge computing services. Other European Opcos taking such hybrid approaches include Deutsche Telekom (DT) and Telefonica.

Conclusions

The use of hybrid cloud and the Vodafone example paint a picture of a cloud journey that cherry picks the best of both worlds. However, there are still few considerations to keep in mind. Hybrid cloud introduces some difficulties and complexities around operating multiple interfaces. This approach may eventually require internal resources to acquire new skills to operate several new cloud technologies. Additionally, hybrid cloud built by hyperscalers will intrinsically consist of some level of proprietary technology. Some in the industry view this as a de facto lock-in.

Since security and service availability are also key concerns preventing many CSPs from the move to public cloud – especially when it comes to core networks – adopting industry-standard approaches and security strategies become key considerations. These can include incorporating the most modern security approaches (e.g. DevSecOps) early in the adoption process.

While it may be more difficult for some operators (potentially smaller CSPs) to disregard the initial cost savings offered by public cloud, many incumbent operators are still reluctant to relinquish their network workloads fully. Among those most vocal about it is US-based MNO Verizon, which suggested it would never put its core networks in public cloud, and European multi-nationals such as DT which also has no plans to move its network functions into the public cloud domain.

This is despite both CSPs having adopted various telco cloud approaches, including hybrid cloud solutions, in telco IT, edge computing and data processing. For wider context it is also worth noting that DT is among the European operator groups spearheading project Sylva, alongside its peers Orange, Telefonica, TIM and Vodafone together with Nordic kit vendors Nokia and Ericsson.

To sum up, despite the TCO savings and operational efficiencies, the majority of CSPs have not initiated a public cloud deployment strategy. By all accounts, when it comes to telco procurement, experienced CSPs may well aim to avoid risking all their resources in one single venture, relinquishing control, and getting cut off from their own assets. Meanwhile, most CSPs introducing public cloud to their networks, it appears, are taking a considered and steady transformational approach. But regardless of public, hybrid, or private, the future of telco networks is eventually headed to the clouds.

Original article can be seen at: